Breaking the MNQ Limit: How Multi-Market Symmetry Boosted Catalyst Performance by 36%

The Challenge of High Volatility

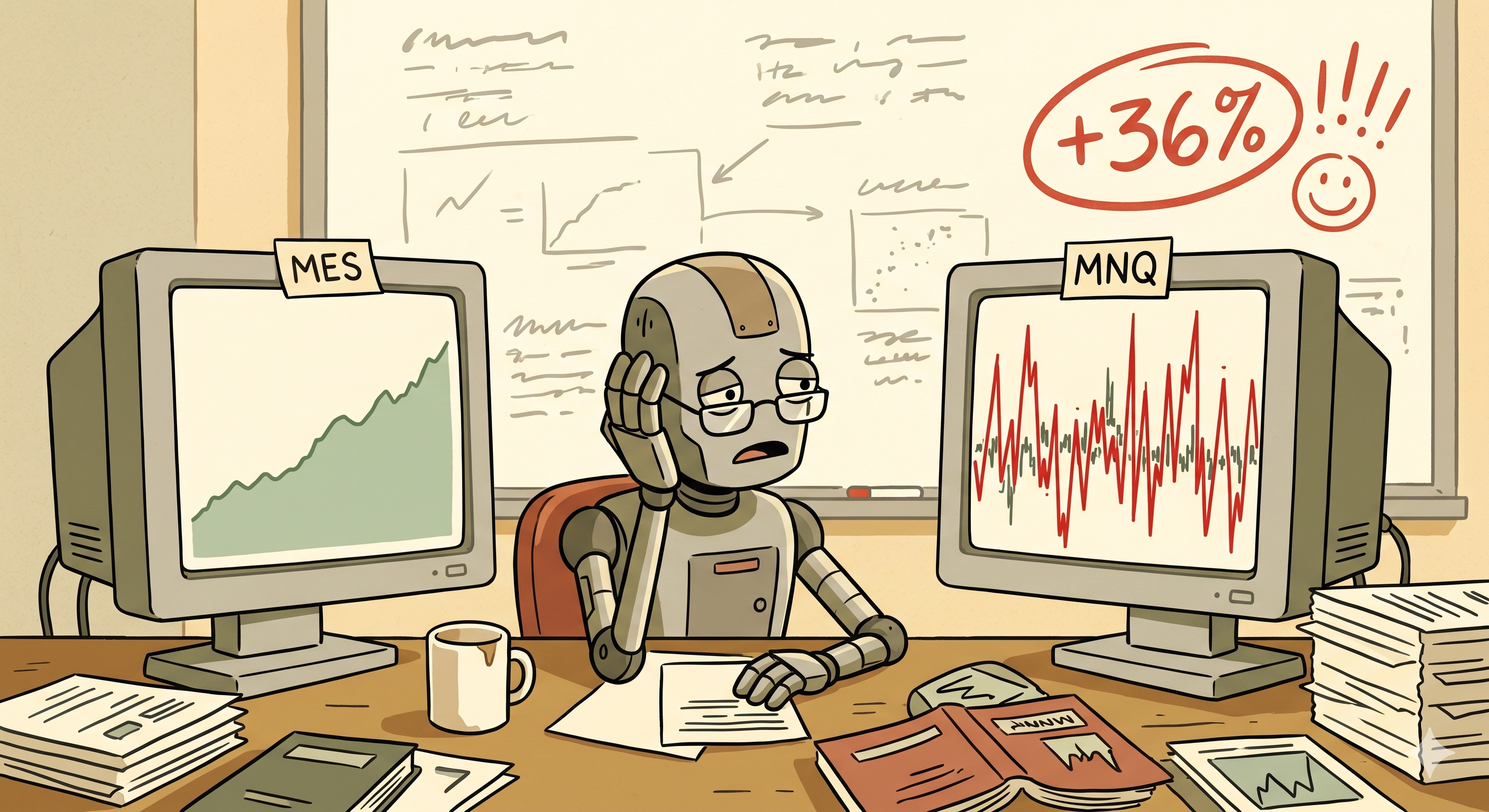

When we launched Catalyst, the system was designed as a surgical execution environment for the Micro S&P 500 (MES). The MES has a noble structure: deep liquidity, predictable behavior at the extremes of the Opening Range (OR), and controlled volatility. However, the community strongly requested a version optimized for the Micro Nasdaq (MNQ).

On paper, it seemed like a natural next step. In practice, optimizing Catalyst for MNQ turned out to be an extremely complex task.

The difficulty lay in two critical factors:

- Finding the Optimal Opening Range (OR): Nasdaq lacks the inertia of the S&P 500. The US session open in the Nasdaq frequently sweeps initial levels with ease due to the aggressive nature of HFT orders.

- Calibrating the Bot to High Volatility Noise: While a 10-12 tick stop loss is statistically viable in the MES, market noise in the MNQ can eat up that space in milliseconds without invalidating the structural direction.

The Search for Algorithmic Symmetry

After thousands of tick-by-tick simulations, we realized that copy-pasting MES configurations to MNQ was a recipe for failure. We had to redesign Catalyst's structural analysis engine for MNQ from scratch.

We increased the absorption filter and expanded the cushion margins based on the adaptive Average True Range (ATR) of the New York pre-market. With these adjustments, the bot was able to survive initial noise spikes. However, the breakthrough did not come from tweaking individual variables, but from running both instruments together in a single portfolio.

"True edge does not lie in mastering a single market, but in exploiting the asymmetry between them."

The Discovery: Combined Trading (MES + MNQ)

Catalyst's historical Achilles' heel has been its low trading frequency; being a highly selective institutional-grade system, it can go days without taking a trade. This poses a psychological and temporal challenge for traders trying to pass prop firm evaluations.

During robustness tests, we decided to run Catalyst simultaneously on MES and MNQ in a single account, but with a non-proportional risk allocation:

- MES (S&P 500): Allocation of 65% of the Maximum Drawdown risk, serving as the consistency anchor.

- MNQ (Nasdaq): Allocation of 35% of the risk, serving as the profit acceleration engine during clean expansions.

The result of this combined approach was a +36% improvement in overall performance (Profit Factor) compared to trading either asset in isolation.

Why Does This Hybrid Model Work?

This non-proportional correlation works for three statistical reasons:

- Drawdown Offsetting: Nasdaq and S&P 500 are highly correlated at a macro level, but diverge in their microstructural timing. Losing streaks rarely overlap in the exact same minute, smoothing the cumulative equity curve.

- Accelerated Target Achievement: By trading both markets, the frequency of valid trades increases substantially without compromising the quality of the entries. This drastically cuts down the time required to pass account evaluations.

- Margin Efficiency: It maximizes the account's purchasing power without over-leveraging on a single, highly volatile asset like Nasdaq.

The deployment of the new templates (both the MNQ-specific ones and the combined MES+MNQ) is now live in the Software Hub. Do not try to fight Nasdaq's volatility in isolation; use multi-market symmetry to your advantage.

Ready to trade with real data?

Stop using retail indicators and switch to institutional order flow.

View SoftwareInner Circle

Join 2,400+ institutional minds. Unfiltered order flow analysis delivered weekly.